Reciba alertas instantáneas cuando salgan noticias sobre sus acciones. Solicite su prueba gratuita de 1 semana para StreetInsider Premium aquí.

Como se presentó ante la Comisión de Bolsa y Valores el 27 de diciembre de 2019

Registro No. 333-163981

Registro No. 811-22356

ESTADOS UNIDOS

COMISIÓN NACIONAL DEL MERCADO DE VALORES

Washington, D.C.20549

FORMULARIO N-1A

DECLARACIÓN DE REGISTRO BAJO LA LEY DE VALORES DE 1933 ☐

Enmienda pre-efectiva No.

☐

Enmienda posterior a la vigencia No. (30)

☒

Y

DECLARACIÓN DE REGISTRO DEBAJO LA LEY DE INVERSIÓN DE 1940 ☐

Enmienda No. (30)

☒

CONFIANZA DE LA SERIE DE INVERSIONES ARCHER

c / o Archer Investment Corporation

9000 Keystone Crossing, Suite 630

Indianápolis, IN 46240

(800) 238-7701

Copias a:

|

Archer Investment Corporation 9000 Keystone Crossing, Suite 630 Indianápolis, IN 46240 (800) 238-7701 |

|

Ley Ropka, LLC 215 Fries Mill Road Turnersville, NJ 08012 (856) 374-1744 |

Se propone que esta presentación sea efectiva:

/ /XX/ inmediatamente después de la presentación de conformidad con el párrafo (b)

/ / / en (_) de conformidad con el párrafo (b)

/ / / 60 días después de la presentación de conformidad con el párrafo (a) (1)

/ / / en

de conformidad con el párrafo (a) (1)

/ / / 75 días después de la presentación de conformidad con el párrafo (a) (2)

/ / / en (fecha) de conformidad con el párrafo (a) (2) de la Regla 485

Si corresponde, marque la siguiente casilla:

/ / / Esta enmienda post-efectiva designa una nueva fecha efectiva para una enmienda post-efectiva presentada previamente.

CONFIANZA DE LA SERIE DE INVERSIONES ARCHER

ARCHER BALANCED FUND – Símbolo de teletipo – ARCHX

ARCHER INGRESOS FONDO – Símbolo de teletipo – ARINX

ARCHER STOCK FUND – Símbolo de teletipo – ARSKX

ARCHER DIVIDEND GROWTH FUND – Símbolo de teletipo – ARDGX

FOLLETO

27 de diciembre de 2019

NOTA IMPORTANTE: a partir del 1 de enero de 2021, según lo permitido por las regulaciones adoptadas por la Comisión de Bolsa y Valores, las copias en papel de los informes de los accionistas del Fondo como este ya no se enviarán por correo, a menos que solicite específicamente copias en papel de los informes el Fondo o de su intermediario financiero, como un corredor de bolsa o banco. En cambio, los informes estarán disponibles en el sitio web del Fondo www.thearcherfunds.com, y se le notificará por correo cada vez que se publique un informe y se le proporcione un enlace al sitio web para acceder al informe.

Si ya eligió recibir informes de accionistas electrónicamente, no se verá afectado por este cambio y no necesita tomar ninguna medida. Puede optar por recibir electrónicamente informes de accionistas y otras comunicaciones del Fondo o de su intermediario financiero llamando o enviando una solicitud por correo electrónico.

Puede elegir recibir todos los informes futuros en papel sin cargo. Puede informar al Fondo o a su intermediario financiero que desea continuar recibiendo copias en papel de sus informes de accionistas llamando o enviando una solicitud por correo electrónico. Su elección de recibir informes en papel se aplicará a todos los fondos mantenidos con el complejo de fondos o su intermediario financiero.

La Comisión de Bolsa y Valores no ha aprobado o desaprobado estos valores ni ha determinado si este prospecto es verdadero o completo. Cualquier representación en contrario es un delito penal.

Tabla de contenido

RESUMEN DEL FONDO

1

ARCHER FONDO EQUILIBRADO

1

Objetivo de inversión

1

Honorarios y gastos de invertir en el fondo

1

Volumen de negocios de cartera

2

Principales estrategias de inversión del fondo

2

Principales riesgos de invertir en el fondo

3

Actuación

6 6

Gestión del fondo

8

Administradores de cartera

8

RESUMEN DEL FONDO

9 9

ARCHER FONDO DE INGRESOS

9 9

Objetivo de inversión

9 9

Honorarios y gastos de invertir en el fondo

9 9

Volumen de negocios de cartera

10

Principales estrategias de inversión del fondo

10

Principales riesgos de invertir en el fondo

11

Actuación

13

Gestión del fondo

14

Administradores de cartera

15

RESUMEN DEL FONDO

dieciséis

ARCHER STOCK FUND

dieciséis

Objetivo de inversión

dieciséis

Honorarios y gastos de invertir en el fondo

dieciséis

Volumen de negocios de cartera

17

Principales estrategias de inversión del fondo

17

Principales riesgos de invertir en el fondo

17

Actuación

18 años

Gestión del fondo

19

Administradores de cartera

20

RESUMEN DEL FONDO

21

ARCHER DIVIDEND FONDO DE CRECIMIENTO

21

Objetivo de inversión

21

Honorarios y gastos de invertir en el fondo

21

Volumen de negocios de cartera

22

Principales estrategias de inversión del fondo

22

Principales riesgos de invertir en el fondo

22

Actuación

25

Gestión del fondo

27

INFORMACIÓN ADICIONAL SOBRE LOS FONDOS

28

OBJETIVOS DE INVERSIÓN, ESTRATEGIAS PRINCIPALES DE INVERSIÓN, RIESGOS RELACIONADOS,

28

Y DIVULGACIÓN DE LAS CARTERAS DE LA CARTERA

28

ARCHER FONDO EQUILIBRADO

28

Objetivo de inversión

28

Principales estrategias de inversión del fondo

28

Principales riesgos de invertir en el fondo

30

Cambio en los objetivos de inversión

33

Posiciones temporales defensivas

33

Divulgación de participaciones de cartera

34

¿Es el fondo adecuado para usted?

34

ARCHER FONDO DE INGRESOS

35

Objetivo de inversión

35

Principales estrategias de inversión del fondo

35

Principales riesgos de invertir en el fondo

36

Cambio en los objetivos de inversión

39

Posiciones temporales defensivas

39

Divulgación de participaciones de cartera

40

¿Es el fondo adecuado para usted?

40

ARCHER STOCK FUND

41

Objetivo de inversión

41

Principales estrategias de inversión del fondo

41

Principales riesgos de invertir en el fondo

41

Cambio en los objetivos de inversión

44

Posiciones temporales defensivas

44

Divulgación de participaciones de cartera

44

¿Es el fondo adecuado para usted?

45

ARCHER DIVIDEND FONDO DE CRECIMIENTO

46

Objetivo de inversión

46

Principales estrategias de inversión del fondo

46

Principales riesgos de invertir en el fondo

46

Posiciones temporales defensivas

50

Divulgación de participaciones de cartera

50

¿Es el fondo adecuado para usted?

50

GESTIÓN, ORGANIZACIÓN Y ESTRUCTURA DE CAPITAL

51

El asesor

51

Los gestores de cartera

52

Pagos a intermediarios y otros intermediarios financieros

53

INFORMACIÓN DEL ACCIONISTA

53

Precio de las acciones del fondo

53

Cómo comprar acciones

54

COMPRA Y VENTA DE ACCIONES DEL FONDO, IMPUESTOS Y COMPENSACIÓN FINANCIERA INTERMEDIA 62

Compra y venta de acciones de fondos

62

Información sobre los impuestos

62

ASPECTOS FINANCIEROS MÁS DESTACADOS

63

ARCHER FONDO EQUILIBRADO

63

ARCHER FONDO DE INGRESOS

64

ARCHER STOCK FUND

sesenta y cinco

ARCHER DIVIDEND FONDO DE CRECIMIENTO

66

POLÍTICA DE PRIVACIDAD

67

CÓMO OBTENER MÁS INFORMACIÓN

68

RESUMEN DEL FONDO

ARCHER FONDO EQUILIBRADO

Objetivo de inversión

El Archer Balanced Fund (el "Fondo") busca el rendimiento total.

Honorarios y gastos de invertir en el fondo

Esta tabla describe los honorarios y gastos que puede pagar si compra y mantiene acciones del Fondo.

|

Honorarios de accionistas (honorarios pagados directamente de su inversión) |

|

|

Tarifa de canje (como un porcentaje del monto canjeado dentro de los noventa (90) días de la compra) |

1,00% |

|

|

|

|

Gastos operativos anuales del fondo (gastos que paga cada año como porcentaje del valor de su inversión) |

|

|

Comisión de gestión |

0,50% |

|

Distribución y / o servicio (12b-1) Tarifas |

Ninguna |

|

Otros gastos |

1.11% |

|

Honorarios y gastos del fondo adquirido (1) |

0.02% |

|

Gastos operativos totales del fondo anual |

1,63% |

|

Exención de tarifas y / o reembolso de gastos (2) |

(0,41%) |

|

Gastos operativos totales del fondo anual después de la exención de tarifas y / o reembolso de gastos |

1,22% |

(1) Los honorarios y gastos del fondo adquiridos representan el gasto proporcional incurrido indirectamente por el fondo como resultado de invertir en fondos del mercado monetario u otras compañías de inversión que tienen sus propios gastos. Los honorarios y gastos no se utilizan para calcular el valor del activo neto del Fondo y no se correlacionan con la relación de Gastos con el Activo neto promedio que se encuentra en la sección "Aspectos financieros más destacados" de este Folleto.

(2) El Asesor acordó contractualmente renunciar a su comisión de gestión y / o reembolsar ciertos gastos operativos del Fondo, pero solo en la medida necesaria para que los gastos operativos totales del Fondo, excluidas las comisiones y comisiones de corretaje, las comisiones 12b-1, los costos por préstamos (como los gastos de intereses y dividendos sobre valores vendidos en corto), impuestos, gastos extraordinarios y cualquier gasto indirecto (como comisiones y gastos de los fondos adquiridos) no exceden el 1,20% del activo neto diario promedio del fondo. De conformidad con el Acuerdo de limitación de gastos, si el Asesor así lo solicita, cualquier gasto operativo del Fondo renunciado o reembolsado por el Asesor de conformidad con el Acuerdo que tuvo el efecto de reducir los Gastos operativos del Fondo al 1,20% en los últimos tres años anteriores a la recuperación. reembolsado al Asesor por el Fondo; siempre que, sin embargo, dicha recuperación no causará que el índice de gastos del Fondo, después de que se haya tenido en cuenta la recuperación, exceda el menor límite de gastos vigente en el momento de la exención o el límite de gastos vigente en el momento de la recuperación . El acuerdo contractual está vigente hasta el 31 de diciembre de 2023. El Acuerdo de Servicios de Gestión puede, con un aviso por escrito de sesenta (60) días, rescindirse con respecto al Fondo, en cualquier momento sin el pago de ninguna multa, por parte de la Junta de Fideicomisarios o por el voto de la mayoría de los valores con derecho a voto en circulación del Fondo, o por la Administración.

Ejemplo:

Este ejemplo tiene la intención de ayudarlo a comparar el costo de invertir en Archer Balanced Fund con el costo de invertir en otros fondos mutuos.

El Ejemplo asume que invierte $ 10,000 en el Fondo durante los períodos de tiempo indicados y luego canjea todas sus acciones al final de esos períodos. El ejemplo también supone que su inversión tiene un rendimiento del 5% cada año y que los gastos operativos del Fondo (que dan efecto a la limitación de gastos solo durante los primeros tres años) siguen siendo los mismos. Aunque sus costos reales pueden ser más altos o más bajos, según estos supuestos, sus costos serían:

1

|

1 AÑO |

3 AÑOS |

5 AÑOS |

10 AÑOS |

|

$ 124 |

$ 474 |

$ 848 |

$ 1,898 |

Volumen de negocios de cartera

El Fondo paga los costos de transacción, como las comisiones, cuando compra y vende valores (o "entrega" su cartera). Una tasa de rotación de cartera más alta puede indicar costos de transacción más altos y puede generar impuestos más altos cuando las acciones del Fondo se mantienen en una cuenta imponible. Estos costos, que no se reflejan en los gastos operativos anuales del fondo o en el ejemplo, afectan el rendimiento del Fondo. Durante el año fiscal más reciente, la tasa de rotación de la cartera del Fondo fue del 13,91% del valor promedio de su cartera.

Principales estrategias de inversión del fondo

El Fondo busca alcanzar su objetivo de rentabilidad total, invirtiendo en una cartera diversificada de valores de renta variable y renta variable. El rendimiento total se compone de ingresos y apreciación del capital. El asesor utiliza un enfoque de arriba hacia abajo para evaluar las industrias y sectores de la economía que están deprimidos o han caído en desgracia con los inversores y luego busca empresas de calidad en esas industrias o sectores que tienen valor en la opinión del asesor. Dentro de cada uno, el asesor busca encontrar compañías con solidez financiera sólida y una administración sólida que vendan por debajo de su valor intrínseco.

Como Fondo equilibrado, en circunstancias normales, el Fondo invertirá hasta un 70%, pero no menos del 25% de sus activos totales en valores de renta variable. El componente de capital de la cartera del Fondo consistirá principalmente en valores de grandes empresas de capitalización (es decir, empresas con capitalizaciones de mercado de más de $ 10 mil millones), pero el Fondo también puede invertir en compañías de pequeña y mediana capitalización si el asesor cree que tales inversiones brindan oportunidades para mayores rendimientos Los valores de renta variable en los que el Fondo puede invertir incluyen principalmente acciones ordinarias, así como valores convertibles en acciones ordinarias y fondos cotizados en bolsa (ETF) que invierten principalmente en valores de renta variable. El Fondo también puede invertir en fideicomisos de inversión inmobiliaria (REIT).

Además, en circunstancias normales, el Fondo invertirá al menos el 30%, pero no menos del 25% de sus activos totales en valores de renta fija, efectivo y equivalentes de efectivo. Los valores de renta fija en los que el Fondo puede invertir incluyen valores emitidos por el gobierno de los EE. UU. Y sus agencias e instrumentos, bonos corporativos, bonos del gobierno extranjero, bonos municipales y bonos de cupón cero, pagarés estructurados y productos similares, REIT de hipotecas, mutuales del mercado monetario fondos y otros instrumentos del mercado monetario, certificados de depósito híbridos y compañías de inversión (como EFT) que invierten principalmente en valores de renta fija. Los valores de renta fija en la cartera del Fondo tendrán principalmente vencimientos de 5 años o menos; sin embargo, de vez en cuando, el Fondo puede invertir en valores de renta fija con vencimientos de hasta 30 años. El Fondo generalmente invierte en títulos de renta fija con calificación de grado de inversión en el momento de la compra (al menos BBB / Baa o superior) según lo determine una de las siguientes organizaciones de calificación :, Fitch Ratings ("Fitch") o Moody's Investors Service, Inc. ("Moody's") o, si no está calificado, determinado por el asesor como de calidad comparable. De vez en cuando, según las condiciones generales del mercado y las perspectivas presentadas por el título individual, el Fondo puede invertir en valores de renta fija sin grado de inversión, comúnmente conocidos como bonos basura. El Fondo no invertirá más del 5% de sus activos en bonos basura (determinado al momento de la compra).

El Fondo puede invertir en valores de renta variable o renta fija de empresas extranjeras que operan en países desarrollados. Los valores de renta variable se limitarán al Depositario estadounidense patrocinado o no patrocinado.

2

Recibos (ADR) negociados en bolsas de valores de EE. UU. Los ADR generalmente son emitidos por un banco estadounidense o una compañía fiduciaria y representan la propiedad de los valores subyacentes emitidos por una compañía extranjera. El Fondo puede perseguir su objetivo de inversión directa o indirectamente invirtiendo en ETF, siempre que dicha inversión se ajuste a las políticas de inversión del Fondo. Al evaluar los ETF, el asesor considera la estrategia de inversión del ETF, la experiencia de su patrocinador, su historial de desempeño, la volatilidad, los datos comparativos de rendimiento y riesgo, el tamaño de los activos y la relación de gastos.

Para fines de gestión de efectivo, el Fondo también puede invertir en instrumentos del mercado monetario a corto plazo y de alta calidad, como obligaciones a corto plazo del gobierno de los EE. UU., Sus agencias o instrumentos, obligaciones bancarias, papel comercial o fondos mutuos del mercado monetario. Al mantener algo de efectivo o equivalentes de efectivo, el Fondo puede evitar darse cuenta de las ganancias y pérdidas de la venta de acciones cuando hay reembolsos de accionistas. Sin embargo, el Fondo puede tener dificultades para cumplir su objetivo de inversión cuando mantiene una posición de efectivo significativa.

El Fondo no buscará obtener ganancias anticipando movimientos del mercado a corto plazo. El asesor tiene la intención de comprar valores que lo cumplan principalmente para los objetivos a largo plazo. Sin embargo, cuando el asesor considere que el cambio beneficiará al Fondo, la rotación de la cartera no será un factor limitante. En consecuencia, los Fondos pueden experimentar una tasa de rotación de cartera superior a la normal.

El Fondo puede vender participaciones que el asesor cree que han reducido el potencial de revalorización del capital y / o ingresos, han tenido un rendimiento inferior al mercado o sus sectores económicos relevantes, han excedido sus valores de mercado justos, han experimentado un cambio en los fundamentos o están sujetos a otros factores que puede contribuir al bajo rendimiento relativo.

Principales riesgos de invertir en el fondo

Los inversores en el Fondo deben tener una perspectiva a largo plazo y, por ejemplo, ser capaces de tolerar disminuciones de valor potencialmente abruptas.

Los precios de los valores en poder del Fondo pueden disminuir en respuesta a ciertos eventos que tienen lugar en todo el mundo, incluidos aquellos que involucran directamente a las compañías cuyos valores son propiedad del Fondo; condiciones que afectan la economía general; cambios generales del mercado; inestabilidad política, social o económica local, regional o global; y fluctuaciones de divisas, tasas de interés y precios de productos básicos. Las acciones ordinarias y otros valores de renta variable comprados por el Fondo pueden implicar grandes oscilaciones de precios y un potencial de pérdida.

Las inversiones en valores emitidos por entidades con sede fuera de los Estados Unidos también pueden verse afectadas por los controles de divisas; diferentes normas y prácticas contables, de auditoría, de informes financieros y legales; expropiación; cambios en la política fiscal; mayor volatilidad del mercado; diferentes estructuras del mercado de valores; mayores costos de transacción; y diversas dificultades administrativas, como retrasos en la compensación y liquidación de las transacciones de cartera o en el pago de dividendos. Estos riesgos pueden aumentar en relación con las inversiones en los mercados emergentes. Las inversiones en valores emitidos por entidades domiciliadas en los Estados Unidos también pueden estar sujetas a muchos de estos riesgos.

Puede perder dinero invirtiendo en el Fondo. El rendimiento del Fondo podría verse afectado por:

Riesgo de gestión. La estrategia de inversión del asesor puede no producir los resultados previstos.

3

Riesgo de la empresa. El valor del Fondo puede disminuir en respuesta a las actividades y perspectivas financieras de una compañía individual en la cartera del Fondo. El valor de una empresa individual puede ser más volátil que el mercado en su conjunto.

Riesgo de valor. El Fondo invierte en valores infravalorados. Es posible que el mercado no esté de acuerdo con la determinación del asesor de que un valor está infravalorado, y el precio del valor puede no aumentar a lo que el asesor cree que es su valor total. Incluso puede disminuir en valor.

Riesgos patrimoniales. Los mercados de valores pueden ser volátiles. En otras palabras, los precios de las acciones pueden aumentar o disminuir rápidamente en respuesta a los acontecimientos que afectan a una empresa o industria específica, o a las cambiantes condiciones económicas, políticas o de mercado. Las inversiones del Fondo pueden disminuir en valor si los mercados bursátiles funcionan mal. También existe el riesgo de que las inversiones del Fondo tengan un rendimiento inferior al de los mercados de valores en general o a segmentos particulares de los mercados de valores.

Riesgo de pequeñas y medianas empresas. Las empresas pequeñas y medianas implican un mayor riesgo de pérdida y fluctuación de precios que las empresas más grandes. Sus valores también pueden ser menos líquidos y más volátiles. Como resultado, el Fondo podría tener mayores dificultades para comprar o vender una garantía de un emisor de micro o pequeña capitalización a un precio aceptable, especialmente en períodos de volatilidad del mercado.

Riesgos de renta fija.

Riesgo crediticio. Es posible que el emisor de una garantía de renta fija no pueda hacer pagos de intereses y capital cuando vencen. En general, cuanto más baja es la calificación crediticia de un valor, mayor es el riesgo de que el emisor incumpla su obligación.

Cambio en el riesgo de calificación. Si una agencia de calificación otorga una calificación de deuda más baja, el valor de la deuda disminuirá porque los inversores exigirán una tasa de rendimiento más alta.

Riesgo de tipo de interés. El valor del Fondo puede fluctuar en función de los cambios en los tipos de interés y las condiciones del mercado. A medida que disminuyen las tasas de interés, el valor de las inversiones del Fondo puede disminuir. Los valores con vencimientos efectivos más largos son más sensibles a los cambios en las tasas de interés que aquellos con vencimientos efectivos más cortos. Además, los emisores de ciertos tipos de valores pueden pagar por adelantado el principal antes de lo programado cuando las tasas de interés aumentan, lo que obliga al Fondo a reinvertir en valores de menor rendimiento. Los pagos de capital más lentos de lo esperado también pueden extender la vida promedio de los valores de renta fija, bloqueando las tasas de interés por debajo del mercado y reduciendo el valor de estos valores.

Riesgo de duración. Los precios de los valores de renta fija con vencimientos efectivos más largos son más sensibles a los cambios en las tasas de interés que aquellos con vencimientos efectivos más cortos.

Riesgo de valores de alto rendimiento. En la medida en que el Fondo invierta en valores de alto rendimiento (bonos basura), estará sujeto a mayores niveles de riesgo de tasa de interés y crédito que los fondos que no invierten en dichos valores. Estos valores se consideran predominantemente especulativos con respecto a la capacidad continua del emisor para realizar pagos de capital e intereses. Una recesión económica podría afectar negativamente al mercado de estos valores y reducir la capacidad del Fondo para vender estos valores (riesgo de liquidez). Si el emisor de un valor está en incumplimiento con respecto a los pagos de intereses o capital, el Fondo puede perder toda su inversión.

Bonos de cupón cero. Se requiere que el Fondo distribuya los ingresos devengados con respecto a los bonos de cupón cero a los accionistas, incluso cuando en realidad no se reciben ingresos por el bono. De vez en cuando, el Fondo

4 4

puede tener que liquidar otros valores de cartera para satisfacer sus obligaciones de distribución en dichos bonos de cupón cero.

Riesgos Extranjeros. En la medida en que el Fondo invierta en valores extranjeros, estará sujeto a riesgos adicionales que pueden aumentar el potencial de pérdidas en el Fondo. Estos riesgos pueden incluir, entre otros, riesgos de país (conflictos políticos, diplomáticos, regionales, terrorismo, guerra, inestabilidad social y económica, devaluaciones de la moneda y políticas que tienen el efecto de limitar o restringir la inversión extranjera o el movimiento de activos), diferentes intercambios prácticas, menos supervisión gubernamental, menos información disponible públicamente, mercados comerciales limitados y mayor volatilidad.

Riesgo de valores de la compañía de inversión. Cuando el Fondo invierte en otras compañías de inversión, como fondos mutuos del mercado monetario o ETF, indirectamente asume su parte proporcional de las comisiones y gastos pagaderos directamente por la otra compañía de inversión. Por lo tanto, el Fondo incurrirá en gastos más altos, muchos de los cuales pueden ser duplicados. Además, el Fondo puede verse afectado por las pérdidas de los fondos subyacentes y el nivel de riesgo derivado de las prácticas de inversión de los fondos subyacentes (como el uso de derivados por parte de los fondos subyacentes). Los ETF también están sujetos a los siguientes riesgos: (i) el precio de mercado de las acciones de un ETF puede negociarse por encima o por debajo de su valor liquidativo; (ii) el ETF puede emplear una estrategia de inversión que utilice altos índices de apalancamiento; o (iv) la negociación de las acciones de un ETF puede detenerse si los funcionarios de la bolsa de valores consideran que dicha acción es apropiada, las acciones se excluyen de la bolsa o la activación de "interruptores de circuito" en todo el mercado (que están vinculados a grandes reducciones en precios de acciones) detiene el comercio de acciones en general. El Fondo no tiene control sobre los riesgos asumidos por los fondos subyacentes en los que invierte.

Riesgo inmobiliario. En la medida en que el Fondo invierta en REIT, está sujeto a riesgos generalmente asociados con la inversión en bienes raíces, tales como (i) posibles disminuciones en el valor de los bienes inmuebles, (ii) condiciones económicas generales y locales adversas, (iii) posible falta de disponibilidad de fondos hipotecarios, (iv) cambios en las tasas de interés y (v) problemas ambientales. Además, los REIT están sujetos a ciertos otros riesgos relacionados específicamente con su estructura y enfoque, tales como: dependencia de las habilidades de gestión; diversificación limitada; los riesgos de localizar y gestionar la financiación de proyectos; fuerte dependencia del flujo de caja; posible incumplimiento por parte de los prestatarios; los costos y posibles pérdidas de autoliquidación de una o más participaciones; la posibilidad de no mantener exenciones del registro de valores; y, en muchos casos, una capitalización de mercado relativamente pequeña, lo que puede resultar en una menor liquidez del mercado y una mayor volatilidad de los precios.

Riesgos de valores gubernamentales.

Riesgo de agencia. Es posible que el gobierno de los EE. UU. No brinde apoyo financiero a sus agencias o instrumentos si la ley no lo exige. Si una agencia o instrumento del gobierno de los EE. UU. En el cual el Fondo invierte incumplimientos y el gobierno de los EE. UU. No respalda la obligación, el precio o el rendimiento de las acciones del Fondo podría caer. Los valores de ciertas entidades patrocinadas por el gobierno de los EE. UU., Como Freddie Mac o Fannie Mae, no son emitidos ni garantizados por el gobierno de los EE. UU.

Sin garantía. La garantía del gobierno de EE. UU. Del pago final del principal y el pago oportuno de intereses sobre ciertos valores del gobierno de EE. UU. Que son propiedad del Fondo no implica que las acciones del Fondo estén garantizadas o que el precio de las acciones del Fondo no fluctúe.

Certificados híbridos de riesgo de depósito. A diferencia de un CD normal, un CD invocable fluctúa en valor. Si las tasas de interés bajan, el CD gana valor; Si las tasas de interés suben, el CD pierde valor. Los CD híbridos suelen ofrecer tasas de interés más altas que las disponibles y, a menudo, tienen vencimientos más largos que los CD normales.

5 5

Riesgo de rotación de cartera. La estrategia de inversión del Fondo puede generar una alta tasa de rotación de la cartera. La alta rotación de la cartera daría lugar a gastos de la comisión de corretaje correspondientemente mayores y podría dar lugar a la distribución a los accionistas de ganancias de capital adicionales a efectos fiscales. Estos factores pueden afectar negativamente el rendimiento del Fondo.

Opción de riesgo. Los movimientos específicos del mercado de una opción y la seguridad subyacente no se pueden predecir con certeza. Cuando el Fondo suscribe una opción de compra cubierta, recibe una prima, pero también renuncia a la oportunidad de beneficiarse de un aumento de precio en el valor subyacente por encima del precio de ejercicio, siempre que su obligación como escritor continúe, y retiene el riesgo de pérdida si el precio de la seguridad disminuye. Otros riesgos asociados con la escritura de opciones de compra cubiertas incluyen la posible incapacidad de efectuar transacciones de cierre a precios favorables y un límite de apreciación de los valores reservados para la liquidación.

Riesgo de notas estructuradas. Los pagarés estructurados están sujetos a una serie de riesgos de renta fija, incluido el riesgo general de mercado, el riesgo de tasa de interés, así como el riesgo de que el emisor del pagaré no pueda realizar los pagos de intereses y / o principal al vencimiento, o puede incumplir sus obligaciones enteramente. Además, como resultado de las características derivadas integradas, las notas estructuradas generalmente están sujetas a un mayor riesgo que invertir en una nota simple o en un bono emitido por el mismo emisor. Es imposible predecir si el factor referenciado (como un índice o tasa de interés) o los precios de los valores subyacentes aumentarán o disminuirán. En la medida en que la porción de renta fija de la cartera del Fondo incluya notas estructuradas, el Fondo puede ser más volátil que otros fondos equilibrados que no invierten en notas estructuradas. Los precios de negociación reales de los pagarés estructurados pueden ser significativamente diferentes del monto principal de los pagarés. Si el Fondo vende las notas estructuradas antes del vencimiento, puede sufrir una pérdida de capital. Al vencimiento final, los pagarés estructurados pueden canjearse en efectivo o en especie, a discreción del emisor. Si las notas se canjean en especie, el Fondo recibiría acciones a un precio deprimido. En la medida en que una nota estructurada no esté protegida por el principal a través de una función de seguro, el principal de la nota no estará protegido.

Riesgo de ciberseguridad. Los incidentes de ciberseguridad pueden permitir que una parte no autorizada tenga acceso a los activos del fondo, a los datos del cliente (incluida la información de los accionistas privados) o a la información de propiedad exclusiva, o puede provocar que el fondo, el administrador, cualquier subasesor y / o sus proveedores de servicios (incluidos, entre otros) , contadores de fondos, custodios, subdepositarios, agentes de transferencia e intermediarios financieros) para sufrir violaciones de datos, corrupción de datos o perder la funcionalidad operativa.

Una inversión en el Fondo no está asegurada ni garantizada por la Federal Deposit Insurance Corporation ni por ninguna otra agencia gubernamental.

El Fondo no es un programa de inversión completo. Al igual que con cualquier inversión de fondos mutuos, los rendimientos del Fondo variarán y podría perder dinero.

Actuación

El siguiente gráfico de barras y las tablas a continuación proporcionan alguna indicación de los riesgos de invertir en el Fondo al mostrar cambios en el rendimiento del Fondo de un año a otro y al mostrar cómo los rendimientos anuales promedio del Fondo durante 1, 5 y 10 años con los de un índice de mercado de base amplia y un promedio de rendimiento de fondos mutuos similares.

Recuerde, el rendimiento pasado del Fondo, antes y después de impuestos, no es necesariamente una indicación de cómo funcionará el Fondo en el futuro. La información de rendimiento actualizada estará disponible llamando al número gratuito del Fondo al 1-800-238-7701.

6 6

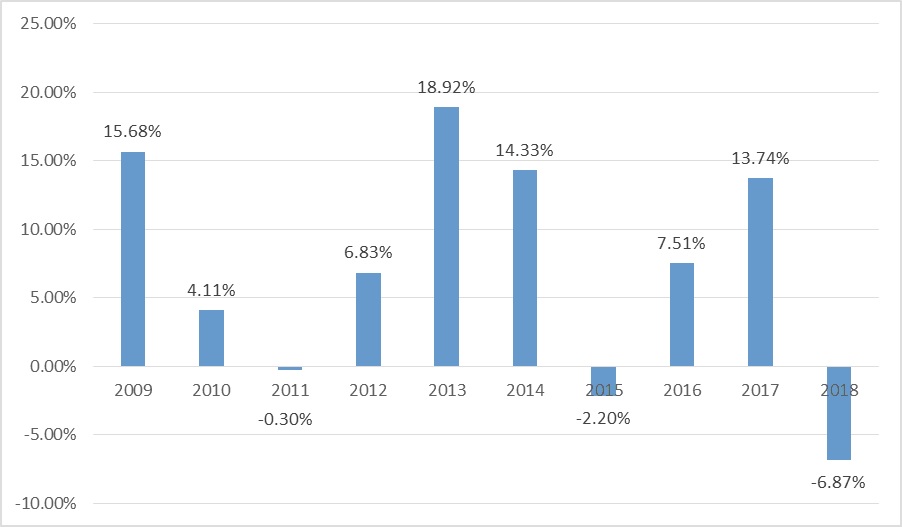

Fondo equilibrado de arquero

El año calendario regresa al 31 de diciembre

La rentabilidad del año calendario hasta la fecha para el Fondo al 30 de septiembre de 2019 fue del 15,46%. Durante el período que se muestra, el rendimiento más alto para un trimestre fue del 12.02% (trimestre finalizado el 30 de junio de 2009); y el rendimiento más bajo fue (14.67)% (trimestre terminado el 31 de diciembre de 2008).

PROMEDIO DE DEVOLUCIONES TOTALES ANUALES

(para los períodos terminados el 31 de diciembre de 2018)

|

El fondo equilibrado |

1 año |

5 años |

10 años |

|

Devolución antes de impuestos |

-6,87% |

4.95% |

6,87% |

|

Devolución después de impuestos sobre distribuciones¹ |

-7,57% |

4,13% |

6.02% |

|

Devolución después de impuestos sobre distribuciones y venta de acciones de fondos¹ |

-3,98% |

3,53% |

5,16% |

|

Índice de cartera estadounidense moderado de Dow Jones (no refleja deducciones por honorarios, gastos o impuestos)2 |

-3,92% |

5,28% |

9,71% |

|

Índice de riesgo objetivo moderado Morningstar3 |

-4,76% |

4.08% |

7,96% |

Returns Las declaraciones después de impuestos se calculan utilizando las tasas históricas más altas de impuestos federales sobre el ingreso marginal individual y no reflejan el impacto de los impuestos estatales y locales o la tasa más baja en las ganancias de capital a largo plazo cuando las acciones se mantienen durante más de 12 meses. Las declaraciones reales después de impuestos dependen de la situación fiscal de un inversor y pueden diferir de las mostradas. Las declaraciones después de impuestos que se muestran no son relevantes para los inversores que poseen sus acciones del Fondo a través de acuerdos con impuestos diferidos, como planes 401 (k) o cuentas de jubilación individuales.

2 El Índice es un punto de referencia no administrado que supone la reinversión de todas las distribuciones y excluye el efecto de impuestos y tarifas. La cartera moderada de Dow Jones es miembro de los índices de riesgo relativo de Dow Jones que mide el rendimiento de las carteras conservadoras, moderadas y agresivas en función de los niveles incrementales de riesgo potencial. Los índices están diseñados para medir sistemáticamente varios niveles de riesgo en relación con el riesgo de un índice de acciones de EE. UU. Los inversores pueden identificar un punto de referencia apropiado como el índice que tiene las características de riesgo histórico más similares.

7 7

3 El Índice de Riesgo Objetivo Moderado de Morningstar es miembro de la Serie de Riesgo Objetivo de Morningstar que abarca el espectro de riesgo de conservador a agresivo. Los índices pueden servir como puntos de referencia para ayudar con la selección y evaluación de fondos mutuos de riesgo objetivo al ofrecer un criterio objetivo para la comparación del rendimiento. Los índices de Morningstar cubren un conjunto global de acciones, bonos y productos básicos, y están diseñados específicamente para ser bloques de construcción ininterrumpidos e invencibles que ofrecen una exposición pura de clase de activos.

Gestión del fondo

Archer Investment Corporation sirve como asesor de inversiones del fondo.

Administradores de cartera

|

Título del fondo profesional de inversiones (si corresponde) |

|

Experiencia con este fondo |

|

Título primario con asesor de inversiones |

|

Troy C. Patton, CPA / ABV |

|

Desde diciembre de 2009; y con el predecesor del Fondo, el Archer Balanced Fund desde 2005 |

|

presidente |

|

Steven Demas |

|

Desde diciembre de 2009 y con el predecesor del Fondo, el Archer Balanced Fund desde abril de 2009 |

|

Vicepresidente sénior |

|

John Rosebrough, CFA |

|

Since November 2010 |

|

Senior Vice President |

For important information about the purchase and sale of fund shares, tax information and financial intermediary compensation, please refer to “Purchase and Sales of Fund Shares, Taxes and Financial Intermediary Compensation” found on Page 62 of this Prospectus.

8

FUND SUMMARY

ARCHER INCOME FUND

Investment Objective

The investment objective of the Archer Income Fund (the “Fund”) is to provide you with current income while secondarily striving for capital appreciation.

Fees and Expenses of Investing in the Fund

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund.

|

Shareholder Fees (fees paid directly from your investment) |

|

|

Redemption Fee (as a percentage of the amount redeemed within 90 days of purchase) |

1.00% |

|

|

|

|

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

|

|

Management Fee |

0.50% |

|

Distribution and/or Service (12b-1) Fees |

None |

|

Other Expenses |

1.18% |

|

Acquired Fund Fees and Expenses (1) |

0.02% |

|

Total Annual Fund Operating Expenses |

1.70% |

|

Fee Waiver and/or expenses reimbursement (2) |

(0.72%) |

|

Total Annual Fund Operating Expenses after Fee Waiver and/or Expense Reimbursement |

0.98% |

(1) Acquired Fund Fees and Expenses represent the pro rata expense indirectly incurred by the Fund as a result of investing in money market funds or other investment companies that have their own expenses. The fees and expenses are not used to calculate the Fund’s net asset value and do not correlate to the ratio of Expenses to Average Net Assets found in the “Financial Highlights” section of this Prospectus.

(2) The Advisor has contractually agreed to waive its management fee and/or reimburse certain Fund operating expenses, but only to the extent necessary so that the Fund’s total operating expenses, excluding brokerage fees and commissions, any 12b-1 fees, borrowing costs (such as interest and dividend expenses on securities sold short), taxes, extraordinary expenses and any indirect expenses (such as Fees and Expenses of Acquired Funds), do not exceed 0.96% of the Fund’s average daily net assets. Pursuant to the Expense Limitation Agreement, if the Adviser so requests, any Fund Operating Expenses waived or reimbursed by the Adviser pursuant to the Agreement that had the effect of reducing Fund Operating Expenses to 0.96% within the most recent three years prior to recoupment shall be repaid to the Adviser by the Fund; provided, however, that such recoupment will not cause the Fund’s expense ratio, after recoupment has been taken into account, to exceed the lesser of the expense cap in effect at the time of the waiver or the expense cap in effect at the time of recoupment. The contractual agreement is in place through December 31, 2023. The Management Services Agreement may, on sixty (60) days’ written notice, be terminated with respect to a Fund, at any time without the payment of any penalty, by the Board of Trustees or by a vote of a majority of the outstanding voting securities of the Fund, or by Management.

Example:

This Example is intended to help you compare the cost of investing in the Archer Income Fund with the cost of investing in other mutual funds.

The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses (giving effect to the

9

expense limitation only during the first three years) remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

|

1 YEAR |

3 YEARS |

5 YEARS |

10 YEARS |

|

$100 |

$312 |

$708 |

$1,816 |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 11.64% of the average value of its portfolio.

Principal Investment Strategies of the Fund

Under normal conditions, at least 50% of the Fund’s total assets will be invested in U.S. government obligations, mortgage and asset-backed securities, corporate and municipal bonds, collateralized mortgage obligations (CMOs), certificates of deposit linked to an index. The securities purchased will be rated BBB or better by either Fitch Ratings (Fitch), or Moody’s Investors Service (Moody’s), or other equivalently rated nationally recognized organization (NRSRO). Further, under normal conditions, up to 20% of the Fund’s total assets will be invested in below investment-grade fixed income securities, commonly referred to as high-yield or “junk” bonds.

The Fund will invest up to 25% of its assets in foreign debt securities denominated in U.S. dollars and foreign currencies. These include foreign fixed income securities issued by corporations and governments and emerging market fixed income securities issued by corporations and governments.

The Fund will invest up to 10% of its assets in covered call options on the debt securities it owns. The Fund will sell covered call options to obtain market exposure or to manage risk or hedge against adverse market conditions. The option is “covered” because the Fund owns the securities at the time it sells the option.

The Fund will invest in fixed income securities primarily through exchange-traded funds ("ETFs") and mutual funds (collectively, the "Underlying Funds") that are not affiliated with the Fund or the advisor. The Fund will invest in ETFs as it may be more cost efficient than investing in individual fixed income securities while gaining exposure to a particular sector or index. An ETF is typically a registered investment company that seeks to track the performance of a particular market index. These indices include not only broad-market indices, but more specific indices as well, including those relating to particular sectors, markets, regions, or industries. An ETF is traded like a stock on a securities exchange and may be purchased and sold throughout the day based on its market price.

When deciding whether to purchase or sell a particular security, the Advisor considers an appraisal of the economy, the relative yields of securities and the investment prospects for issuers. The Advisor also, carefully assesses the particular security’s yield-to-maturity, credit quality, liquidity, call risk and current yield.

10

The Fund will invest in a broad range of fixed income instruments without benchmark constraints or significant sector/instrument limitations.

Principal Risks of Investing in the Fund

Investors in the Fund should have a long-term perspective and, for example, be able to tolerate potentially sharp declines in value.

The prices of securities held by the Fund may decline in response to certain events taking place around the world, including those directly involving the companies whose securities are owned by the Fund; conditions affecting the general economy; overall market changes; local, regional, or global political, social, or economic instability; and currency, interest rate and commodity price fluctuations. The common stock and other equity type securities purchased by the Fund may involve large price swings and potential for loss.

Investments in securities issued by entities based outside the United States may also be affected by currency controls; different accounting, auditing, financial reporting, and legal standards and practices; expropriation; changes in tax policy; greater market volatility; differing securities market structures; higher transaction costs; and various administrative difficulties, such as delays in clearing and settling portfolio transactions or in receiving payment of dividends. These risks may be heightened in connection with investments in emerging markets. Investments in securities issued by entities domiciled in the United States may also be subject to many of these risks.

You may lose money by investing in the Fund. The Fund’s performance could be hurt by:

Issuer Risk. Securities held by the Fund may decline in value because of changes in the financial condition of or other events affecting, the issuers of these securities.

Asset-Backed Securities Investment Risk. The Fund may run the risk that the impairment of the value of the assets underlying a security in which the Fund invests such as non-payment of loans, will result in a reduction in the value of the security.

Management Risk. The advisor’s judgments about the attractiveness, value and potential appreciation of a particular asset class or individual security in which the Fund invests may prove to be incorrect and there is no guarantee that the advisor’s or sub-advisor’s judgments will produce the desired results.

Interest Rate Risk. When the Fund invests in bonds or in Underlying Funds that own bonds, the value of your investment in the Fund will fluctuate with changes in interest rates. Typically, a rise in interest rates causes a decline in the value of bond funds owned by the Fund. In general, the market price of debt securities with longer maturities will increase or decrease more in response to changes in interest rates than shorter-term securities.

Credit Risk. A security’s price may decline due to deterioration in the issuer’s financial condition, or the issuer may fail to repay interest and/or principal in a timely manner. The risk is higher for below investment grade bonds.

Call Risk. During periods of falling interest rates, issuers of callable bonds may repay securities with higher interest rates before maturity. This could cause the Fund to lose potential price appreciation if it reinvests the proceeds at lower interest rates.

11

Liquidity Risk. If the Fund invests in illiquid assets, or if asset become illiquid there may be no willing buyer of the securities and the Fund may have to sell those securities at a lower price or may not be able to sell the securities at all each of which would have a negative effect on performance.

ETF Risk. The Fund will incur higher and duplicative expenses when it invests in Underlying Funds. There is also the risk that the Fund may suffer losses due to the investment practices of the Underlying Funds (such as the use of derivatives). The ETFs in which the Fund invests may not be able to replicate exactly the performance of the indices they track, due to transactions costs and other expenses of the underlying funds. The shares of closed-end funds frequently trade at a discount to their net asset value. Accordingly, there can be no assurance that the market discount on shares of any closed-end fund purchased by the Fund will ever decrease, and it is possible that the discount may increase.

Mortgage Backed Securities Risk. Mortgage-backed securities have several risks, including:

– credit and market risks of mortgage-backed securities: the mortgage loans or the guarantees underlying the mortgage-backed securities may default or otherwise fail leading to non-payment of interest and principal.

– prepayment risk of mortgage-backed securities: in times of declining interest rates, the Fund’s higher yielding securities may be prepaid and the Fund will have to replace them with securities having a lower yield.

– extension risk of mortgage-backed securities: in times of rising interest rates mortgage prepayments will slow causing portfolio securities considered short or intermediate term to be long-term securities which fluctuate more widely in response to changes in interest rates than shorter term securities.

– inverse floater, interest- and principal-only securities risk: these securities are extremely sensitive to changes in interest rates and prepayment rates.

– illiquidity of mortgage markets: the mortgage markets are currently facing additional economic pressures such as the devaluation of the underlying collateral, increased loan underwriting standards which limits the number of real estate purchasers, and excess supply of properties in certain geographic regions, which puts additional downward pressure on the value of real estate in these regions.

Foreign Risk. Investments in foreign securities may be affected by currency controls and exchange rates; different accounting, auditing, financial reporting, and legal standards and practices; expropriation; changes in tax policy; greater market volatility; differing securities market structures; higher transaction costs; and various administrative difficulties, such as delays in clearing and settling portfolio transactions or in receiving payment of dividends. These risks may be heightened in connection with investments in emerging or developing countries.

Foreign Currency Risk. To the extent the Fund invests in securities or Underlying Funds that hold securities that are denominated in foreign currencies, the value of securities denominated in foreign currencies can change significantly when foreign currencies strengthen or weaken relative to the U.S. dollar. Currency rates in foreign countries may fluctuate significantly over short periods of time for a number of reasons, including changes in interest rates and the imposition of currency controls or other political developments in the U.S. or abroad. These currency movements may negatively impact the value of the Fund even when there is no change in the value of the security in the issuer’s home country.

12

Emerging Markets Risk. Countries with emerging markets may have relatively unstable governments, social and legal systems that do not protect shareholders, economies based on only a few industries, and inefficient securities markets

Junk Bonds Risk. Investments in junk bonds involve a greater risk of default and are subject to a substantially higher degree of credit risk or price changes than other types of debt securities. These securities are considered speculative because they have a higher risk of issuer default, are subject to greater price volatility and may be illiquid.

General Fixed-Income Securities Risk. The market prices of bonds, including those issued by the U.S. government, go up as interest rates fall, and go down as interest rates rise. As a result, the net asset value of the Fund will fluctuate with conditions in the bond markets. In the case of corporate bonds and commercial paper, values may fluctuate as perceptions of credit quality change. In addition, investment grade bonds may be downgraded or default. During periods of declining interest rates, or for other reasons, bonds may be “called,” or redeemed, by the bond issuer prior to the bond’s maturity date, resulting in the Fund receiving payment earlier than expected. This may reduce the Fund’s income if the proceeds are reinvested at a lower interest rate.

Government Securities Risk. Economic, business, or political developments may affect the ability of government sponsored guarantors to repay principal and to make interest payments on the securities in which the Fund invests. In addition, certain of these securities, including those issued or guaranteed by FNMA (Federal National Mortgage Association, or Fannie Mae) and FHLMC (Federal Home Loan Mortgage Corporation, or Freddie Mac), are not backed by the full faith and credit of the U.S. government.

Municipal Securities Risk. Municipal Securities can be significantly affected by political changes as well as uncertainties in the municipal market related to taxation, legislative changes, or the rights of municipal security holders.

Cybersecurity Risk. Cybersecurity incidents may allow an unauthorized party to gain access to fund assets, customer data (including private shareholder information), or proprietary information, or cause the fund, the manager, any subadviser and/or its service providers (including, but not limited to, fund accountants, custodians, sub-custodians, transfer agents and financial intermediaries) to suffer data breaches, data corruption or lose operational functionality.

Your investment in the fund is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency, entity or person.

Performance

The following bar chart and tables below provide some indication of the risks of investing in the Fund by showing changes in the Fund’s performance from year to year and by showing how the Fund’s average annual returns for 1, 5, and 10 years with those of a broad-based market index and a performance average of similar mutual funds.

Remember, the Fund’s past performance, before and after taxes, is not necessarily an indication of how the Fund will perform in the future. Updated performance information will be available by calling the Fund toll-free at 1-800-238-7701.

13

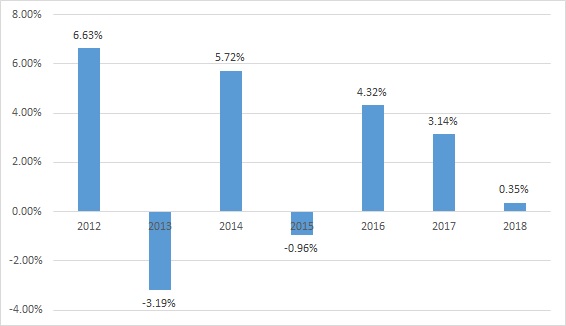

Archer Income Fund

Calendar Year returns as of December 31

The calendar year-to-date return for the Fund as of September 30, 2019, was 5.45%. During the period shown, the highest return for a quarter was 3.36% (quarter ended March 31, 2014); and the lowest return was (3.05)% (quarter ended June 30, 2013).

AVERAGE ANNUAL TOTAL RETURNS

(for the periods ended December 31, 2018)

|

The Income Fund |

1 Year |

5 Years |

Since Inception (3/11/2011) |

|

Return Before Taxes |

0.35% |

2.48% |

2.58% |

|

Return After Taxes on Distributions¹ |

-0.80% |

1.22% |

1.21% |

|

Return After Taxes on Distributions and Sale of Fund Shares¹ |

0.20% |

1.33% |

1.40% |

|

Barclay’s Capital U.S. Aggregate Bond Index (reflects no deductions for fees, expenses, or taxes)2 |

0.01% |

2.52% |

2.79% |

¹ After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes or the lower rate on long-term capital gains when shares are held for more than 12 months. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts.

2 The Index is an unmanaged benchmark that assumes reinvestment of all distributions and excludes the effect of taxes and fees. The Barclay's Capital U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including U.S. Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS, and CMBS. The U.S. Aggregate Index was created in 1986.

14

Management of the Fund

Archer Investment Corporation serves as the Investment Advisor of the Fund.

Portfolio Managers

|

Investment Professional Fund Title (if applicable) |

|

Experience with this Fund |

|

Primary Title with Investment Advisor |

|

Troy C. Patton, CPA/ABV |

|

Since March 2011 |

|

President |

|

Steven Demas |

|

Since March 2011 |

|

Senior Vice President |

|

John Rosebrough, CFA |

|

Since March 2011 |

|

Senior Vice President |

For important information about the purchase and sale of fund shares, tax information and financial intermediary compensation, please refer to “Purchase and Sales of Fund Shares, Taxes and Financial Intermediary Compensation” found on Page 62 of this Prospectus.

15

FUND SUMMARY

ARCHER STOCK FUND

Investment Objective

The investment objective of the Archer Stock Fund (the “Fund”) is capital appreciation.

Fees and Expenses of Investing in the Fund

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund.

|

Shareholder Fees (fees paid directly from your investment) |

|

|

Redemption Fee (as a percentage of the amount redeemed within ninety (90) days of purchase) |

1.00% |

|

|

|

|

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

|

|

Management Fee |

0.50% |

|

Distribution and/or Service (12b-1) Fees |

None |

|

Other Expenses |

1.24% |

|

Acquired Fund Fees and Expenses(1) |

0.01% |

|

Total Annual Fund Operating Expenses |

1.75% |

|

Fee Waiver and/or expenses reimbursement (2) |

(0.51%) |

|

Total Annual Fund Operating Expenses after Fee Waiver and/or Expense Reimbursement |

1.24% |

1 Acquired Fund Fees and Expenses represent the pro rata expense indirectly incurred by the Fund as a result of investing in money market funds or other investment companies that have their own expenses. The fees and expenses are not used to calculate the Fund’s net asset value and do not correlate to the ratio of Expenses to Average Net Assets found in the “Financial Highlights” section of this Prospectus.

2The Advisor has contractually agreed to waive its management fee and/or reimburse certain Fund operating expenses, but only to the extent necessary so that the Fund’s total operating expenses, excluding brokerage fees and commissions, any 12b-1 fees, borrowing costs (such as interest and dividend expenses on securities sold short), taxes, extraordinary expenses and any indirect expenses (such as Fees and Expenses of Acquired Funds), do not exceed 1.23% of the Fund’s average daily net assets. Pursuant to the Expense Limitation Agreement, if the Adviser so requests, any Fund Operating Expenses waived or reimbursed by the Adviser pursuant to the Agreement that had the effect of reducing Fund Operating Expenses to 1.23% within the most recent three years prior to recoupment shall be repaid to the Adviser by the Fund; provided, however, that such recoupment will not cause the Fund’s expense ratio, after recoupment has been taken into account, to exceed the lesser of the expense cap in effect at the time of the waiver or the expense cap in effect at the time of recoupment. The contractual agreement is in place through December 31, 2023. The Management Services Agreement may, on sixty (60) days’ written notice, be terminated with respect to a Fund, at any time without the payment of any penalty, by the Board of Trustees or by a vote of a majority of the outstanding voting securities of the Fund, or by Management.

Example:

This Example is intended to help you compare the cost of investing in the Archer Stock Fund with the cost of investing in other mutual funds.

The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses (giving effect to the expense limitation only during the first three years) remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

16

|

1 YEAR |

3 YEARS |

5 YEARS |

10 YEARS |

|

$126 |

$393 |

$797 |

$1,927 |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 95.51% of the average value of its portfolio.

Principal Investment Strategies of the Fund

Under normal market conditions, the Fund will invest in a portfolio of common stocks and equity securities which include preferred stock and depository receipts of companies of all sizes. The Advisor employs security selection based on research and analysis of the company’s historical data. In selecting securities to purchase, the Advisor evaluates factors that include, but are not limited to: market capitalization, valuation metrics, and earnings and price momentum over time. Portfolio securities may be sold generally upon periodic rebalancing of the Fund’s portfolio. The Advisor considers the same factors it uses in evaluating a security for purchase and generally sells securities when it believes such securities no longer meet its investment criteria.

The Fund will invest up to 30% of its total assets in the securities of foreign issuers, including those in emerging markets, and will invest up to 10% of its total assets in real estate investment trusts (“REITS”) or foreign real estate companies. The Advisor expects that the Fund’s investment strategy may result in a portfolio turnover rate in excess of 100% on an annual basis.

Principal Risks of Investing in the Fund

Investors in the Fund should have a long-term perspective and, for example, be able to tolerate potentially sharp declines in value.

The prices of securities held by the Fund may decline in response to certain events taking place around the world, including those directly involving the companies whose securities are owned by the Fund; conditions affecting the general economy; overall market changes; local, regional, or global political, social, or economic instability; and currency, interest rate and commodity price fluctuations. The common stock and other equity type securities purchased by the Fund may involve large price swings and potential for loss.

Investments in securities issued by entities based outside the United States may also be affected by currency controls; different accounting, auditing, financial reporting, and legal standards and practices; expropriation; changes in tax policy; greater market volatility; differing securities market structures; higher transaction costs; and various administrative difficulties, such as delays in clearing and settling portfolio transactions or in receiving payment of dividends. These risks may be heightened in connection with investments in emerging markets. Investments in securities issued by entities domiciled in the United States may also be subject to many of these risks.

You may lose money by investing in the Fund. The Fund’s performance could be hurt by:

17

Market Risk. Overall stock market risks may also affect the value of the Fund. Factors such as domestic economic growth and market conditions, interest rate levels and political events affect the securities markets.

Small and Mid-Cap Risk. Direct investments in individual small capitalization companies may be more vulnerable than larger, more established organizations to adverse business or economic developments. In particular, small capitalization companies may have limited product lines, markets, and financial resources and may be more dependent upon a relatively small management group.

Foreign Securities Risk. Investments in foreign securities may be affected by currency controls and exchange rates; different accounting, auditing, financial reporting, and legal standards and practices; expropriation; changes in tax policy; greater market volatility; differing securities market structures; higher transaction costs; and various administrative difficulties, such as delays in clearing and settling portfolio transactions or in receiving payment of dividends. These risks may be heightened in connection with investments in emerging or developing countries.

Real Estate Risks. The value of Equity REITs may be affected by changes in the value of the underlying property owned by the REITs, while the value of mortgage REITs may be affected by the quality of any credit extended. Investment in REITs involves risks similar to those associated with investing in small capitalization companies, and REITs (especially mortgage REITs) are subject to interest rate risks. Because REITs incur expenses like management fees, investments in REITs also add an additional layer of expenses

Active Trading Risk. Active trading could raise transaction costs (thus lowering return). In addition, active trading could result in increased taxable distributions to shareholders and distributions that will be taxable to shareholders at higher federal income tax rates.

Equity Risk. Equity securities generally have greater price volatility than fixed income securities.

Management Risk. The advisor’s investment strategy may fail to produce the intended results. The Advisor’s management practices and investment strategies might not work to meet the Fund’s investment objective.

Cybersecurity Risk. Cybersecurity incidents may allow an unauthorized party to gain access to fund assets, customer data (including private shareholder information), or proprietary information, or cause the fund, the manager, any subadviser and/or its service providers (including, but not limited to, fund accountants, custodians, sub-custodians, transfer agents and financial intermediaries) to suffer data breaches, data corruption or lose operational functionality.

Performance

The following bar chart and tables below provide some indication of the risks of investing in the Fund by showing changes in the Fund’s performance from year to year and by showing how the Fund’s average annual returns for 1, 5, and 10 years with those of a broad-based market index and a performance average of similar mutual funds.

Remember, the Fund’s past performance, before and after taxes, is not necessarily an indication of how the Fund will perform in the future. Updated performance information will be available by calling the Fund toll-free at 1-800-238-7701.

18

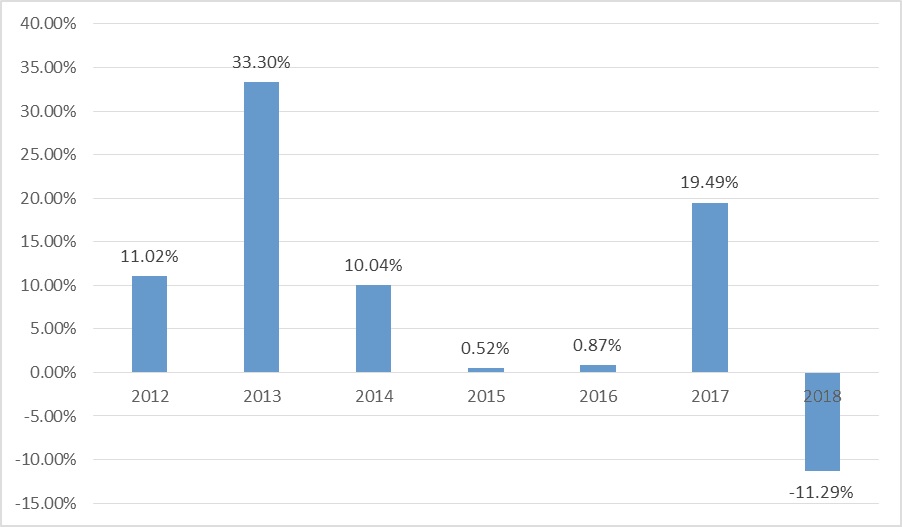

Archer Stock Fund

Calendar Year returns as of December 31

The calendar year-to-date return for the Fund as of September 30, 2019, was 14.56%. During the period shown, the highest return for a quarter was 12.34% (quarter ended March 31, 2012); and the lowest return was (18.14)% (quarter ended December 31, 2018).

AVERAGE ANNUAL TOTAL RETURNS

(for the periods ended December 31, 2018)

|

The Stock Fund |

1 Year |

5 Years |

Since Inception (3/11/2011) |

|

Return Before Taxes |

-11.29% |

3.41% |

6.11% |

|

Return After Taxes on Distributions¹ |

-11.89% |

2.78% |

5.50% |

|

Return After Taxes on Distributions and Sale of Fund Shares¹ |

-6.26% |

2.61% |

4.74% |

|

S&P 500 Index (reflects no deductions for fees, expenses, or taxes)2 |

-4.38% |

8.49% |

11.02% |

¹ After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes or the lower rate on long-term capital gains when shares are held for more than 12 months. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts.

19

2 The Index is an unmanaged benchmark that assumes reinvestment of all distributions and excludes the effect of taxes and fees. The Standard & Poor’s 500 Index (“S&P 500”) is a market value-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. The S&P 500 is a widely recognized, unmanaged index of common stock prices. The figures for the S&P 500 reflect all dividends reinvested but do not reflect any deductions for fees, expenses or taxes.

Management of the Fund

Archer Investment Corporation serves as the Investment Advisor of the Fund.

Portfolio Managers

|

Investment Professional Fund Title (if applicable) |

|

Experience with this Fund |

|

Primary Title with Investment Advisor |

|

Troy C. Patton, CPA/ABV |

|

Since March 2011 |

|

President |

|

Steven Demas |

|

Since March 2011 |

|

Vice President |

|

John Rosebrough, CFA |

|

Since March 2011 |

|

Senior Vice President |

For important information about the purchase and sale of fund shares, tax information and financial intermediary compensation, please refer to “Purchase and Sales of Fund Shares, Taxes and Financial Intermediary Compensation” found on Page 62 of this Prospectus.

20

FUND SUMMARY

ARCHER DIVIDEND GROWTH FUND

Investment Objective

The Archer Dividend Growth Fund (the “Fund”) seeks to provide income and, as a secondary focus, long-term capital appreciation.

Fees and Expenses of Investing in the Fund

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund.

|

Shareholder Fees (fees paid directly from your investment) |

|

|

Redemption Fee (as a percentage of the amount redeemed within ninety (90) days of purchase) |

1.00% |

|

|

|

|

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

|

|

Management Fee |

0.50% |

|

Distribution and/or Service (12b-1) Fees |

None |

|

Other Expenses |

1.22% |

|

Acquired Fund Fees and Expenses(1) |

0.21% |

|

Total Annual Fund Operating Expenses |

1.93% |

|

Fee Waiver and/or expenses reimbursement(2) |

(0.74)% |

|

Total Annual Fund Operating Expenses after Fee Waiver and/or Expense Reimbursement |

1.19% |

(1)

Acquired Fund Fees and Expenses represent the pro rata expense indirectly incurred by the Fund as a result of investing in money market funds or other investment companies that have their own expenses. The fees and expenses are not used to calculate the Fund’s net asset value and do not correlate to the ratio of Expenses to Average Net Assets found in the “Financial Highlights” section of this Prospectus.

(2)

The Advisor contractually has agreed to waive its management fee and/or reimburse certain Fund operating expenses, but only to the extent necessary so that the Fund’s total operating expenses, excluding brokerage fees and commissions, any 12b-1 fees, borrowing costs (such as interest and dividend expenses on securities sold short), taxes, extraordinary expenses and any indirect expenses (such as Acquired Funds Fees and Expenses), do not exceed 0.98% of the Fund’s average daily net assets. Pursuant to the Expense Limitation Agreement, if the Adviser so requests, any Fund Operating Expenses waived or reimbursed by the Adviser pursuant to the Agreement that had the effect of reducing Fund Operating Expenses to 0.98% within the most recent three years prior to recoupment shall be repaid to the Adviser by the Fund; provided, however, that such recoupment will not cause the Fund’s expense ratio, after recoupment has been taken into account, to exceed the lesser of the expense cap in effect at the time of the waiver or the expense cap in effect at the time of recoupment. The contractual agreement is in place through December 31, 2023. The Management Services Agreement may, on sixty (60) days’ written notice, be terminated with respect to a Fund, at any time without the payment of any penalty, by the Board of Trustees or by a vote of a majority of the outstanding voting securities of the Fund, or by Management. The Management Services Agreement shall automatically terminate in the event of its assignment. The Expense Limitation Agreement may only be terminated by the Board of Trustees on sixty (60) days' written notice to Management or upon the termination of the Management Services Agreement between the Trust and Advisor.

Example:

This Example is intended to help you compare the cost of investing in the Archer Dividend Growth Fund with the cost of investing in other mutual funds.

21

The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses (giving effect to the expense limitation only during the first three years) remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

|

1 YEAR |

3 YEARS |

5 YEARS |

10 YEARS |

|

$121 |

$378 |

$823 |

$2,061 |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 19.29% of the average value of its portfolio.

Principal Investment Strategies of the Fund

Under normal market conditions, the Fund seeks to achieve its objective to provide income and, as a secondary focus, long-term capital appreciation, by investing at least 80% of its net assets in equity securities of large-capitalization companies, primarily in dividend-paying equity securities, consisting of common stocks, preferred stocks and shares of beneficial interest of real estate investment trusts ("REITs"). These companies have market capitalizations in the range $500 million and up. The market capitalization range and composition of the companies in the Fund are subject to change. The Fund invests primarily in common stocks of companies that the investment manager believes have the potential to pay above-average, stable dividend and long-term, above-average earnings growth. The Fund may from time to time emphasize one or more economic sectors in selecting its investments, including the consumer discretionary, health care, and information technology and technology-related sectors.

The Fund may invest up to 30% of its total assets in foreign securities. The Fund may invest directly in foreign securities or indirectly through depositary receipts.

The Fund may continue to own a security as long as the dividend or interest yields satisfy the Fund's objectives, and the Adviser believes the valuation is attractive and industry trends remain favorable. Once the Advisor believes a security does not meet the long-term objectives of the fund, it may sell the securities.

Principal Risks of Investing in the Fund

The Archer Dividend Growth Fund is subject to management risk and the Fund may not achieve its objective if the Advisor’s expectations regarding particular securities or interest rates are not met.

An investment in this Fund or any other fund may not provide a complete investment program. The suitability of an investment in the Fund should be considered based on the investment objective, strategies and risks described in this prospectus, considered in light of all of the other investments in your portfolio, as well as your risk tolerance, financial goals and time horizons. You may want to consult with a financial advisor to determine if this Fund is suitable for you.

22

Investors in the Fund should have a long-term perspective and, for example, be able to tolerate potentially sharp declines in value.

The prices of securities held by the Fund may decline in response to certain events taking place around the world, including those directly involving the companies whose securities are owned by the Fund; conditions affecting the general economy; overall market changes; local, regional or global political, social or economic instability; and currency, interest rate and commodity price fluctuations. The common stock and other equity type securities purchased by the Fund may involve large price swings and potential for loss.

Investments in securities issued by entities based outside the United States may also be affected by currency controls; different accounting, auditing, financial reporting, and legal standards and practices; expropriation; changes in tax policy; greater market volatility; differing securities market structures; higher transaction costs; and various administrative difficulties, such as delays in clearing and settling portfolio transactions or in receiving payment of dividends. These risks may be heightened in connection with investments in emerging markets. Investments in securities issued by entities domiciled in the United States may also be subject to many of these risks.

Your investment in the fund is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency, entity or person.

You may lose money by investing in the Fund. The Fund’s performance could be hurt by:

Active Management Risk. Due to its active management, the Fund’s performance could underperform its benchmark index and/or other funds with similar investment objectives.